Have you done your 2024 Strategic Planning yet? Chances are very high that you did—now it’s time for you to review what you planned versus the latest results from the Households Welfare Monitoring Survey for Zimbabwe.

The latest Round 10 survey shows access to basic food necessities shocks due to various factors, chief of which is inflation and affordability. It also shows the currency use by households and the main sources of income at household level.

The economy is now almost full dollarized and this will bring in new opportunities and risks. Neighbouring countries likely to be lured by the greenback and flood our streets with their products. Enterprising Zimbabweans to also venture more into import opportunities. Will there be currency reforms to reverse the dollarization? There are already plans in place if we are to go by recent currency reforms. However once a country crosses the Rubicon of Dollarization—almost impossible to reverse.

Anyway some o f the highlights include the following;

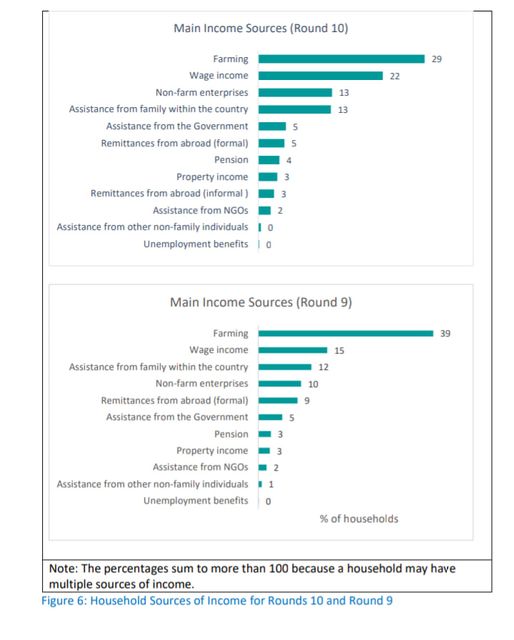

The main source of income for households are 1.Farming, followed by 2.Salaries and 3. Non farming Enterprises. In your business plan—you should have captured the above 3 income line items. For instance if you have a vehicle servicing business—are you capturing farmers in targeted marketing? If you are an NGO—do you have farming as one of your programs?

Farming and Non Farming Enterprises account for 42% of income for households in Zimbabwe which is twice the income coming from salaries. This shows the rise in impact of the small businesses in the country.

Formal and informal diaspora remittances account for 8% of households income. Therefore for every dollar circulating in the economy, at least 10 cents is officially from outside the country. A very important benchmark for business planning as some of the decision makers at household level are based outside the country. Are you targeting the diaspora in your marketing campaigns?

The country doesn’t have unemployment benefits—which is worrisome as NGOs are contributing a paltry 2% to household income and 5% is coming from the government. However the gap is being filled by family members assistance which is at 13%0. There is a gap for insurance companies and banks to create pensions and small businesses.

Not much coming from property income and therefore projections from the wealth taxes not expected to significantly contribute to the fiscus.

Perhaps time to tweak your focused outputs in 2024 and worryingly, the nation continues to experience inflation shocks despite significant dollarization moves.

![]()